Capco: Partnership platform – Christopher Geldard

Driven by new regulation and connected customers, the rise of APIs and open banking is set to fundamentally transform the financial services industry. How, though, should the regulations be implemented and how can banks deliver API products that offer valuable customer experiences? Christopher Geldard and the Capco team provide their insight.

Compared with other industries, the digital revolution has been relatively slow to transform banking but, when the EU introduces its new Payment Services Directive II (PSD2) regulation in 2018, many expect that to change. The regulation, which enables authorised third parties to access key customer data from banks and initiate payments on behalf of a customer will, according to Christopher Geldard, managing partner at Capco, "fundamentally change the landscape of banking as we know it".

From an industry Geldard describes as "siloed not only by business units but also by products", the new world of application programming interfaces (APIs) will create a fresh, connected network of financial institutions and third-party providers with a whole new ecosystem of banking service apps and improved customer experiences. It's fair to say that most regulations, at least since the financial crisis, haven't offered something that exciting.

"The nice thing about what's happening is that the regulation is actually driving a growth agenda," says Geldard. "Regulations over the past four to five years have all been about reducing risk. This, on the other hand, is about genuine business expansion."

From conversations had by Jeffrey Tijssen, head of fintech and digital partnerships at Capco, banks are now beginning to recognise that PSD2 is much more than an exercise in compliance.

"Initially, most banks did consider this to be yet another regulatory initiative," he says. "Now, however, many have realised that PSD2 actually offers a massive opportunity for banks. It can create new revenue streams to unlock innovation within and outside an organisation, and is a tremendous opportunity to partner with some of the leading fintech start-ups to provide a much better customer experience. I think it is one of the most interesting pieces of new regulation that we have seen for a long time."

How to benefit

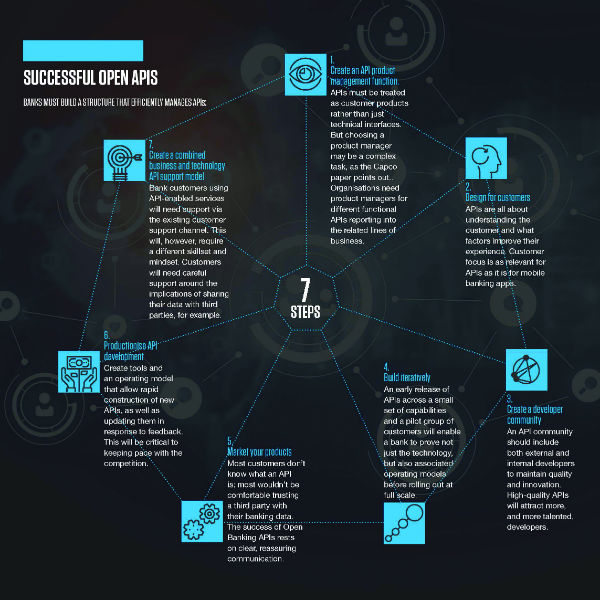

For forward-thinking banks looking to benefit from PSD2, the key according to Jack Burrows, principal consultant at Capco Digital, is treating APIs like any other customer product. "Banks need to ensure that what they deliver is optimised for the customer," he says. "The customer experience of these APIs will be just as important as that of a bank's mobile banking app." How should this be done? According to Burrows, there are a number of points to consider. "The first thing is to create an API product management function where you have a product manager acting as the voice of the customer and the business who is always there to ensure that what is delivered is the right thing for them both," he adds.

"The second point is to design for customers, which means talking to third-party companies and developers that are using that API, and existing bank customers. Third, there is a real imperative that banks cultivate a developer community to build new experiences for their customers with these APIs. That means there is a need to attract the best developers, who can create high-quality experiences."

While the first regulatory deadline for PSD2 is not until 2018, delivering ahead of time is key, Burrows adds, if banks want to unlock business value and also learn from their mistakes. "If they genuinely think that APIs are going to provide new, valuable customer experiences, why would they wait until the regulatory date to do it?" he asks. "Working ahead of schedule means banks can learn from real customer feedback and then modify the product as they go, rather than wait for a big bang in 2018."

One challenge for banks implementing APIs will be building a combined business and technology support model that is capable of actually supporting them. "Most banks have previously used APIs simply as technical interfaces to connect one system to another," Burrows says. "Now they are going to be customer products, which means they need to be supported by business and technology. If the API goes down, for example, you need someone in technology to fix it. If you have a customer who has a question or a concern about using an API, they need to be able to ring and speak to someone. Building such an operating model is as big a challenge, if not bigger, than actually building these APIs.

Once the APIs and support models are built, banks and regulators will also face the challenge of marketing them. As things stand, few customers are aware of what APIs actually are and are therefore unlikely to be comfortable trusting third parties with their secure data. "The success of open banking and PSD2 is really going to depend on how banks and regulators communicate open APIs to their customers," says Burrows. "If it is not communicated well, and people don't know how to use them safely and securely, it could end up being a bit of a white elephant that nobody actually uses."

Share the wealth

Banks are also going to have to get used to sharing data - sometimes with groups they might not want to. "They are going to have to work with other banks and with non-banks," says Geldard. "This is one of the key ramifications of open banking, PSD2 and the idea of the 'connected consumer'. Sharing data with utility companies and tech companies is one thing. Seeing how banks actually co-exist and share data between themselves will be very interesting. Why, for example, would the top four want to share with the likes of Virgin, Metro Bank and so forth? Why would they want to give a leg-up to challenger banks?"

For Tijssen, if banks want to overcome these challenges and deliver APIs that provide new, valuable customer experiences, collaboration will be key. "Partnerships will be absolutely instrumental if open banking is going to be a success," he says. "There are so many advantages to working with fintech start-ups: they are all building APIs that can accelerate the process for banks. I also think we are moving towards this concept of banking as a platform. Rather than developing products themselves, banks will form partnerships with fintech players to provide best-in-class customer experiences. At Capco, one of the things we've developed is something called Capco Connect. It is an ecosystem of different start-ups that we can introduce to the banks."

As the world of open banking and PSD2 approaches, Capco believes it has a lot to offer the financial services industry.

"We've got great experience of designing and delivering customer products and propositions for banks over many years," Burrows says. "We've really taken that experience and those techniques and applied it to APIs. I think that is our real differentiator."

The consultancy firm has already successfully helped implement APIs in a number of banks, Tijssen adds: "We are working with a Tier-1 bank in the UK, on the design and delivery of its PSD2 and open banking programmes."

"We are also working on something similar with a global bank, where we are building a state-of-the-art banking platform, which is again underpinned by APIs. The bank in question has really put API development at the heart of what they wanted to do. In addition to building the actual platform, we are also working with our fintech partners and a number of software providers to develop the APIs and deliver the programme."

Perhaps most importantly for Tijssen, though, is maintaining that product mindset and helping banks at every stage in their API journey. "At Capco, we see APIs as products, and we have the skills and capabilities in house to not just build them for our clients but also to look at the entire operating model that comes with it," he says. "Capco's track record in creating original customer experiences means we are uniquely positioned to support banks that want to take advantage of this opportunity. It's not just about implementing the regulation but also providing customers with a truly transparent and personalised way to manage their money."